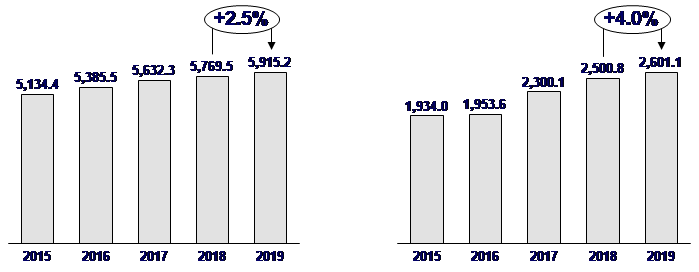

Abu Dhabi, UAE – 12 February 2020: Abu Dhabi Islamic Bank (ADIB), a leading Islamic bank in the region, announced a growth of 4% in net profit to AED 2,601.1 million. Operating Profit increased 4.4% to AED 3,262.2 million, driven by a 3.1% growth in customer financing to AED 81.1 billion, a 30.7% increase in investment income to AED 687.0 million and a 23.6% rise in foreign exchange income to AED 317.5 million. Group net revenues increased by 2.5% in 2019 to AED 5,915.2 million.

Key Financial Highlights

- Group net profit for 2019 increased by 4.0% to AED 2,601.1 million vs. AED 2,500.8 million in 2018. Group net revenues for 2019 grew by 2.5% to AED 5,915.2 million vs. AED 5,769.5 million in 2018 due to growth in customer finance and higher investment and foreign exchange income.

- Net profit margin was 4.25%, despite lower rates in the market, helped by the positive impact of the low cost of funds and a growth in customer financing.

- Operating expenses at AED 2.6 billion were flat year-on-year, reflecting cost discipline initiatives that led to a decrease of 1% in cost to income ratio. This was achieved despite investments in key strategic and digital initiatives designed to support business growth, enhance customer experience and create future efficiencies .

- Total assets as of 31 December 2019 were AED 125.9 billion, representing an increase of 0.6% from AED 125.2 billion at the end of 31 December 2018.

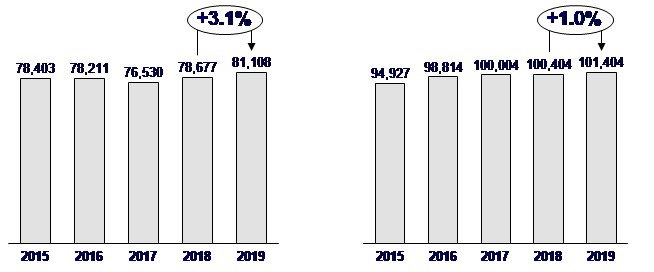

- Net customer financing increased by 3.1% to AED 81.1 billion from AED 78.7 billion at the end of 31 December 2018.

- Credit provisions and impairments for 2019 increased by 6.1% to AED 658.1 million vs. AED 620.1 million in 2018, with net cost of risk increasing to an annualised 78 bps.

- CASA deposits increased by AED 1.7 billion (2.5% increase year on year) to AED 69.8 billion as at 31 December 2019, comprising 69% of the 101.4 billion total customer deposits compared to 67.8% a year earlier.

- Our advances to stable funds ratio increased in Q4 2019 to 84.1% from 82.9% at 31 December 2018 reflecting our ability to make optimal use of the balance sheet.

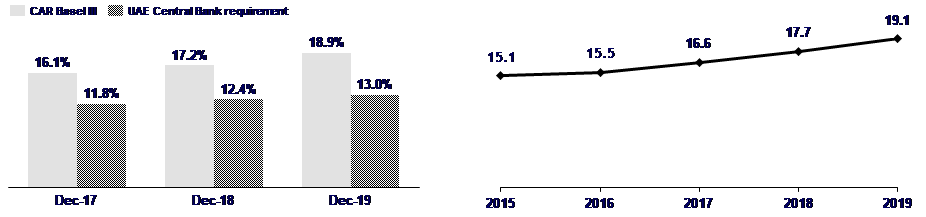

- The bank’s common equity tier 1 ratio of 13.11% and capital adequacy ratio of 18.88% remains well above minimum requirements.

Group Financial highlights – Two year performance

| As at 31 December | All figures are in AED millions |

|---|

|

Balance sheet |

2018 |

2019 |

Change % |

| Total assets | 125,194 | 125,987 | 0.6% |

| Gross customer financing | 81,559 | 84,121 | 3.1% |

| Customer deposits | 100,404 | 101,404 | 1.0% |

| Total equity | 17,737 | 19,103 | 7.7% |

| Customer financing to deposit ratio | 78.4% | 80.0% | |

|

Income statement |

2018 |

2019 |

Change % |

| Net revenue | 5,769 | 5,915 | 2.5% |

| Operating profit (margin) | 3,126 | 3,262 | 4.4% |

| Credit provisions and impairment charge | 620 | 658 | 6.1% |

| Net profit after zakat & tax | 2,501 | 2,601 | 4.0% |

| Stage 3 financing to gross financing assets ratio | 4.8% | 6.5% | |

| Cost to income ratio | 45.8% | 44.9% | |

|

|

Group net revenues – AED million |

Group net profit – AED million |

Management comment

On behalf of the Board of Directors and the management team, Mr. Mazin Manna, ADIB Group CEO, said: “Our 2019 earnings of AED 2.6 billion with a 4% growth marked a steady finish to 2019 in which we increased revenue across our core businesses while maintaining strong expense discipline throughout the organization. At a time when competition in the banking industry has intensified, we were able to grow our revenues reflecting successful business strategies and product propositions. This underlying performance, coupled with progress in our long-term strategic initiatives, helped us generate a significant return on shareholder value of 18.6%.”

“Our growth in revenues has been complemented by our discipline in managing costs which saw the cost to income ratio decrease by almost 1% for the year. We have demonstrated strong expense discipline across the bank and successfully implemented a number of optimization initiatives, resulting in a flat expense base. However, the full financial benefits of these initiatives have been partially offset by investments in new digital and strategic initiatives that can help to attract new customers and support ADIB’s long-term growth.”

“Our retail banking division delivered a solid performance in 2019, supported by a rise in net financing income and growth in fee income, driven by cards and wealth management products. In our wholesale banking business, we continued to build on a strong track record in financing and advisory, supporting clients in capital markets, M&A advisory, syndicated financing, cash management and global trade services. New business deals have led to a healthy growth in our asset book despite the challenging market backdrop. We have strengthened our digital capabilities with the rollout of several new Transaction Banking products and services, such as ADIB Direct and ADIB Office Banking which provides customers with remote access banking solutions.

“Despite a low rate environment, our net profit margin was 4.25%, helped by the positive impact of a low cost of funds that is supported by higher CASA balances. Our liquidity remains strong, with an advances-to-deposits ratio increasing in Q4 19 to 80% reflecting our ability to make optimal use of the balance sheet.”

“The bank has completed the first year of its digital transformation plan launching a number of new services and features in 2019, including adding new features to our mobile banking experience enabling pre-approved customers to receive funds instantly, apply for a card or update KYC instantly from the app. Our enhanced mobile app has driven growth of 20% in our mobile user base compared to last year where over 60% of our customers are now using digital channels. In 2020, we will continue to advance the Bank’s digital credentials, introduce new products and convenient banking solutions that improve the banking experience for all our customers.”

Outlook

“Despite challenges in the macroeconomic environment, the prospects for the UAE in 2020 are encouraging as the Government’s stimulus plans and Expo 2020 are expected to boost key economic sectors. ADIB will continue to invest in areas where we see opportunities for customer growth, particularly through a concerted focus on enhancing our digital banking services. We have a five-year strategic plan that will make ADIB a stronger, more efficient, better-structured bank that is well-positioned to pursue growth opportunities across all of our businesses. By adhering to this plan and focusing on delivering an exceptional banking experience to our customers, we are confident that we will continue to deliver the performance our shareholders have come to expect in 2020 and beyond.”

Key performance indicators

Risk management

As per IFRS 9, customer financing classified under Stage 3 stands at 6.5% with these assets now totaling AED 5,440.2 million. Furthermore, total credit provisions held under IFRS 9 stood at AED 3,013.2 million at the end of 2019. Credit provisions and impairments for 2019 increased by 6.1% to AED 658.1 million vs. AED 620.1 million for 2018.

Asset and Liability Management

ADIB recorded a healthy customer financing-to-deposits ratio of 80.0% as at 31 December 2019. The bank maintained its position as one of the liquid financial institutions in the UAE. Customer financing assets increased 3.1% year on year.

|

|

Net Customer Financing Growth – AED million |

Customer Deposit Growth - AED million |

Capital strength

Total equity (including Tier 1 capital instruments) was AED 19.1 billion at 31 December 2019. This represents an increase of 7.7% year-on-year.

ADIB’s capital adequacy ratio under Basel III as at 31 December 2019 was 18.88%, while its Tier 1 capital ratio was at 17.79% and its common equity Tier 1 ratio stood at 13.11%. All capital ratios under Basel III principles are above the minimum regulatory thresholds advised by Central Bank of the UAE.

|

|

Capital Adequacy Ratio - % |

Total Equity – AED billion |

Cost management

Operating expenses were flat year-on-year, reflecting cost discipline initiatives that led to a decrease of 1% in cost to income ratio. This was achieved despite ADIB’s focus on putting in place the necessary infrastructure to support its growth strategy. Specifically, ADIB has continued to enhance its digital capabilities across all businesses and processes. The bank is enhancing service and convenience, while building and diversifying its fee income capabilities in line with identified customer needs .

ADIB is also upgrading all aspects of its infrastructure to ensure the bank functions efficiently in a stable and secure operating environment.

Business Highlights

- The retail banking group delivered a strong performance in 2019 supported by growth in customer financing and fee income. The cards franchise was strengthened with the launch of ADIB Emirates Skywards cards that offer customers the opportunity to earn Skywards Miles.

- The bank continued to advance its digitisation agenda with ongoing enhancements of the mobile app including launching “Express Finance” service, which provides qualifying customers with instant access to personal finance, KYC update through the app and mobile application through the card. Tablet kiosks were also launched in branches to allow customers to rapidly update their information.

- ADIB revealed a new digital banking proposition targeting millennials called Smartbanking. Smartbanking features digital onboarding and a range of innovative products delivered through a dedicated mobile banking app and intuitive online banking platform.

- ADIB has unveiled a savings plan called “Khuttati” to encourage medium to long-term investments through regular contributions.

- ADIB wholesale banking group was involved in arranging multibillion dollar in structured and syndicated finance deals on behalf of clients. This has led to a growth in our asset book. Furthermore, ADIB advised a number of issuers on optimizing their capital and financing requirements and acted as a Joint Lead Manager & Bookrunner on a number of high profile Sukuk mandates.

- ADIB also upgraded its transaction banking and trade finance proposition with the launch of “ADIB Direct”, a new digital banking platform for businesses that integrates a suite of banking solutions into a single, streamlined interface. The platform includes ADIB Office Banking, which provides a number of remote access solutions, such as cheque printing, cheque scanning, alongside other services, all of which allow ADIB customers to enjoy fast and secured 24/7 banking experience without leaving their office.

- From a Group Risk and Compliance standpoint, ADIB is committed to maintaining high standards of risk governance and risk culture by applying best-in-class risk-management practices to respond to evolving regulation, changes in customer behavior, and the deployment of new technology.

Approvals

These results are subject to approval by the Central Bank of the UAE and shareholders at ADIB’s Annual General Assembly.

ADIB Group financial summary – Three month and Full Year summary

|

Financials |

Q4 2018 |

Q4 2019 |

Chg Q4 2019 vs. Q4 2018 |

2018 |

2019 |

Chg 2019 vs. 2018 |

| |

AED Mn |

AED Mn |

% |

AED Mn |

AED Mn |

% |

| Net Revenue from Funding | 1,078.1 | 953.1 | -11.6% | 3,906.7 | 3,818.3 | -2.3% |

| Fees & Commissions | 314.5 | 335.6 | 6.7% | 1,058.7 | 1,083.3 | 2.3% |

| Investment income | 161.2 | 144.8 | -10.2% | 525.5 | 687.0 | 30.7% |

| FX | 59.1 | 88.8 | 50.4% | 257.0 | 317.5 | 23.6% |

| Other | 2.4 | 2.1 | -11.9% | 21.7 | 9.2 | -57.6% |

|

Total Revenues |

1,615.3 |

1,524.4 |

-5.6% |

5,769.5 |

5,915.2 |

2.5% |

|

Total Expenses |

733.0 |

667.6 |

-8.9% |

2,643.8 |

2,653.1 |

0.4% |

|

Operating profit (margin) |

882.3 |

856.8 |

-2.9% |

3,125.7 |

3,262.2 |

4.4% |

| Credit Provisions and Impairment | 133.1 | 105.6 | -20.6% | 620.1 | 658.1 | 6.1% |

|

Net Profit before Zakat & Tax |

749.2 |

751.2 |

0.3% |

2,505.6 |

2,604.1 |

3.9% |

| Zakat & Tax | 0.9 | 0.5 | -41.2% | 4.8 |

3.0 | -38.8% |

|

Net Profit after Zakat & Tax |

748.3 |

750.6 |

0.3% |

2,500.8 |

2,601.1 |

4.0% |

| Total Assets (in AED Billion) | 125.2 | 125.9 | 0.6% | 125.2 | 125.9 | 0.6% |

| Customer Financing (in AED Billion) | 78.7 | 81.1 | 3.1% | 78.7 | 81.1 | 3.1% |

| Customer Deposits (in AED Billion) | 100.4 | 101.4 | 1.0% | 100.4 | 101.4 | 1.0% |